Top Credit Card Issuers in the US

- American Express: Known for exceptional service and premium travel rewards, AmEx cards are ideal for consumers who want top-tier perks and are comfortable with higher credit standards.

- Capital One: Offering everything from secured cards to premium travel options, Capital One is a favorite for Americans seeking flexible rewards and user-friendly mobile banking tools.

- Discover: Recognized for its rotating cash back categories and U.S.-based customer service, Discover is often chosen by students and credit-builders alike.

- Chase: Chase cards come with generous welcome bonuses, premium rewards programs, and trusted fraud protection — a go-to for travel enthusiasts and everyday spenders.

- Navy Federal Credit Union: Serving military families, Navy Federal offers competitive APRs, low fees, and solid rewards, making it a strong contender for eligible members seeking personalized service.

Major Bank Credit Cards

Major bank cards are widely available from U.S. institutions like Chase, Citi, and Bank of America. These credit cards offer substantial rewards programs, long 0% APR periods, and high credit limits — perfect for well-qualified applicants. However, they often require strong credit scores and can include annual fees. These cards are a top choice for maximizing travel points, balance transfer offers, and long-term benefits but might not suit those rebuilding credit.

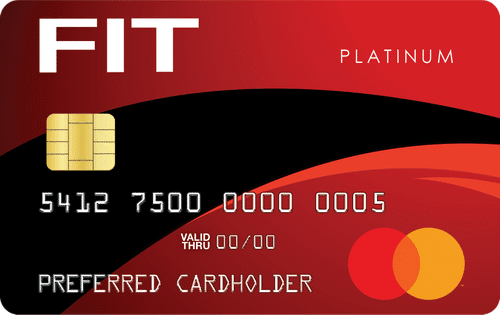

FIT Mastercard Credit Card

The FIT Mastercard, issued by The Bank of Missouri, is tailored for individuals in the U.S. who need help building or repairing their credit history. This unsecured card provides a $400 initial credit limit, with a possible increase to $800 after six months of responsible usage. It doesn’t require a security deposit and reports monthly to all three major credit bureaus. While it includes a setup and annual fee, the card’s value lies in its accessibility and potential for long-term credit improvement. With 24/7 online account access, fraud liability protection, and tools for monitoring your progress, the FIT Mastercard is an empowering option for Americans aiming to boost their FICO scores.

Fintech or Online-Only Credit Card Issuers

Fintech credit card providers like Tomo, Chime, and Petal offer innovative products that use alternative underwriting and modern technology to serve underserved consumers. These issuers often eliminate traditional credit checks and provide budgeting tools, instant alerts, and app-based customer support. Though they typically offer lower limits and may lack travel perks, they are highly attractive to younger or tech-savvy Americans who want transparency and control over their finances.

Secured Credit Cards for Building Credit

Secured cards are widely used in the U.S. by consumers looking to build credit from scratch. These require a refundable security deposit and often match your credit limit to that amount. Popular choices like the Capital One Secured and Discover it® Secured offer credit-building benefits, reporting to credit bureaus, and even cash back in some cases. They serve as a stepping stone for future unsecured cards and often come with educational resources to improve financial literacy.

Retail Store Credit Cards

Retail credit cards are offered by stores like Macy’s, Best Buy, or Walmart and often feature sign-up discounts and exclusive sales. However, they tend to have high interest rates and limited usage—only applicable within that store or retail group. In the U.S., these cards are easier to obtain but should be used carefully to avoid high balances that can impact your credit score and cost you more than the benefits they provide.

How Credit Cards Impact Your Finances and Credit Score in the US

Understanding how credit cards work in the U.S. is essential to long-term financial health. Keeping your credit utilization low—ideally below 30%—helps your FICO score improve. On-time payments are the biggest contributor to a positive credit history, while carrying balances can result in compounding interest charges. Your DTI ratio also matters when applying for large loans like mortgages.

Balance transfers can help manage existing debt but must be used wisely. Benefits like extended warranties, fraud protection, and travel coverage add value, but too many hard inquiries from frequent applications can hurt your score. Smart card management means knowing your terms, paying off balances when possible, and viewing credit as a financial tool, not a burden.

Chase Ink Business Credit Card <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'> Discover why the Chase Ink Business Credit Card is a top choice for U.S. small business owners, offering strong cash back rewards, flexible benefits, and business-focused financial tools.</p>

Chase Ink Business Credit Card <p class='sec-title' style='line-height: normal; font-weight: normal;font-size: 16px !important; text-align: left;margin-top: 8px;margin-bottom: 0px !important;'> Discover why the Chase Ink Business Credit Card is a top choice for U.S. small business owners, offering strong cash back rewards, flexible benefits, and business-focused financial tools.</p>